$HRBR outlook

Continue to be bullish on upgauging, United arbitration, and attractive valuation

Earnings are due today 11/14, but a delay may be expected similar to last quarter. This update is a small summary of what I expect operationally and why I continue to be bullish at this price.

Operating Performance

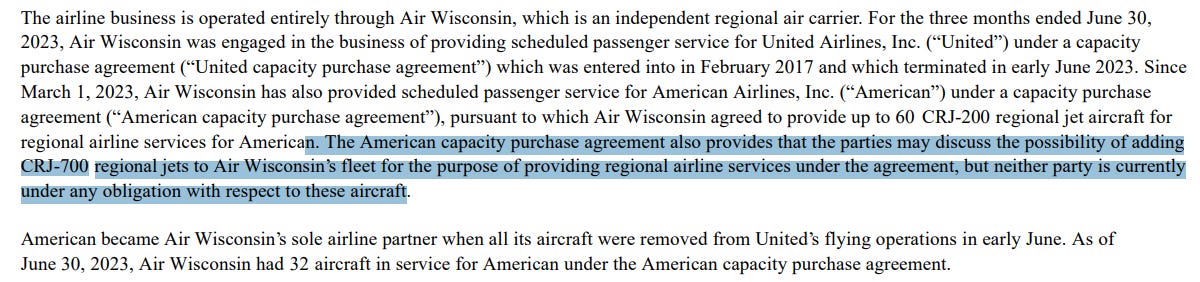

Q3 performance is expected to mirror recent quarters due to the termination of the United contract and lower volume in the exclusive American contract beginning April 2023, featuring fewer up to a capacity of 60 CRJ200s (of which 32 are currently operating). Historical seasonality effects may also affect performance immaterially.

In the meantime throughout, management has continued to buyback stock at roughly the same pace between $2.00 - $2.50.

Bullish at Current Valuation

As of writing at $1.92 close, I maintain a very bullish stance based on the valuation vs risk profile, plus new indications from scuttlebutting around pilot forums, and a potential third upside vector from the United contingency payout which should resolve shortly.

Attractive valuation and risk profile

The risk-reward profile, while more precarious due to AA contract timing uncertainties, still remains highly attractive. In the downside case where the contract stagnates, downsizing OpEx provides a mitigation strategy if they fail to upgauge with American. On the other hand, the upside potential, contingent on significant upgauging, represents a target price at the very minimum of $3-4 and potentially far beyond if the capacity picks up significantly, but the upside time and value are hard to pinpoint exactly, unfortunately.

Regarding valuation, at $1.92 per 43.2m f/d shares out, the implied enterprise value for common, given cash equivalents + ST Investment of $157m, $66m debt, and $13m pref, is a WHOPPING $3.2m. Meanwhile the 60 CRJ-200’s on the balance sheet marked to a net $105m in the last 10Q are worth at the very bare minimum of $1m each on the open market, more likely $2m-5m each. Therefore I’m very comfortable with this share price.

Positive indications from pilots

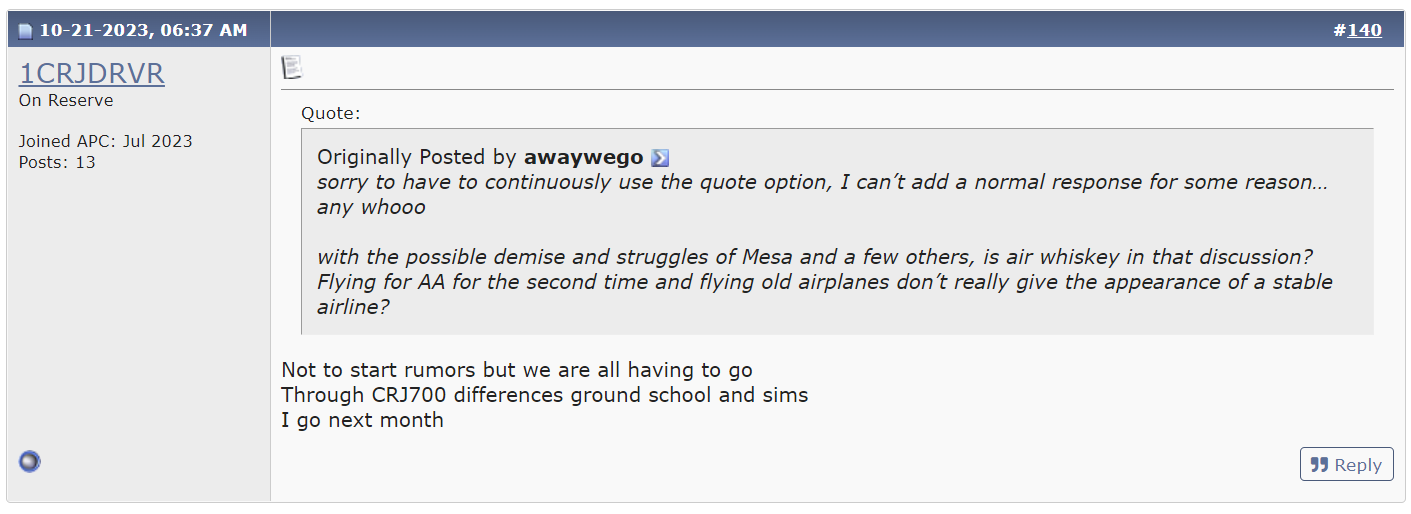

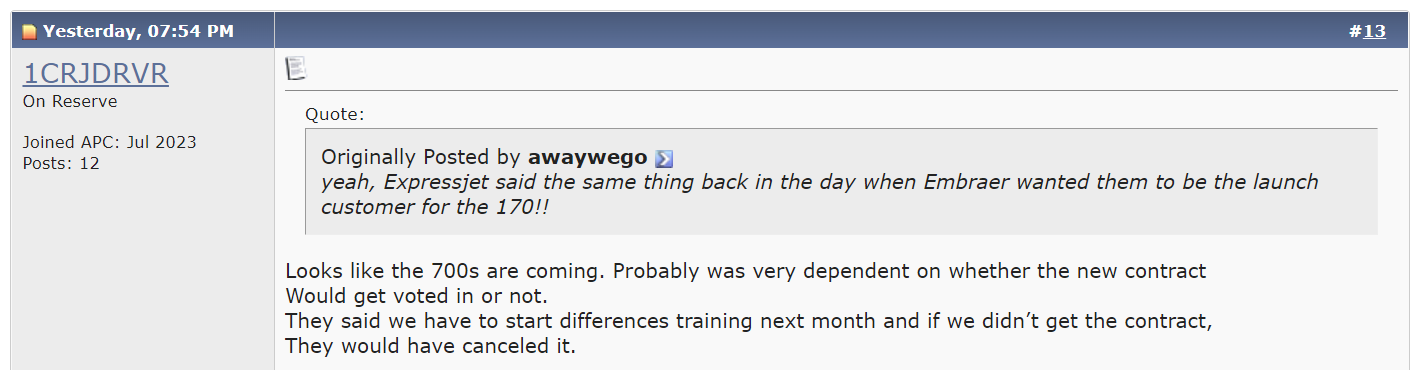

Secondly, the below tidbits from pilot forums suggest to me that the Air Wisconsin team is preparing pilots to fly larger planes and potentially expand their contract with AA. They are adding mandatory differences training for Air Wisconsin pilots is continuing to take place, indicating potential preparation for upgauging to larger CRJ700 jets.

New pay bands are also emerging, further signaling again the potential for new larger planes and/or routes.

In addition, I actually take HRBR NOT reducing OpEx during this interim period as another indication that they intend to continue the business with more and larger planes.

Another upside leg from arbitration

Lastly, the continued arbitration with United which has already dragged performance down in the recent quarters due to legal fees, is expected to resolve in Q4 (or perhaps already resolved in Q3). Full resolution to the upside is worth $52m–I don’t have a strong legal opinion other than I would be very very surprised if exactly $0 is won by HRBR here, so feel free to add your own probability adjusted value from this dispute on top of what was discussed above.

Conclusion: Upside/Risk profile remains attractive, but timing is less certain

Overall, HRBR's current limbo presents an investment opportunity with potentially asymmetric upside in excess of $3-4 share price at the minimum with very limited downside.

The downside price floor is supported by the asset value of their 60 planes, since the open market value of the planes (at least $60-120m at the minimum) is far far higher than the measly enterprise value of $3.2m currently implied by the $1.92 stock price. Secondly, the strategic shift towards larger CRJ700s potentially signaled by pilot forum discussions adds further likelihood to the upside, while the upcoming Q4 resolution of the $52m United arbitration provides a third upside leg worth up to $1.20/sh.

So they got $0 money from United in the arbitration. How does this change your valuation of the company?

The stock only trade about $40k USD per day on average. If I buy $4k, that’s 10% of ADV. how do you accumulate a stock like this?