$HRBR 2021 Q3 Update

New base case following UAL decision as likely scenarios crystallize further

Firstly—appreciate everyone’s patience, I recently started a new job so have been really busy.

The latest update was post-Q2 and left off here:

Background on the company is outlined in the above post so I’ll get to the Q3 update.

The takeaway is: the distribution of valuation scenarios has narrowed since United opted NOT to renew the capacity agreement in 2023, such that the new 2023 liquidation base case is ~30% above the current price with several upside options we are paying nothing for.

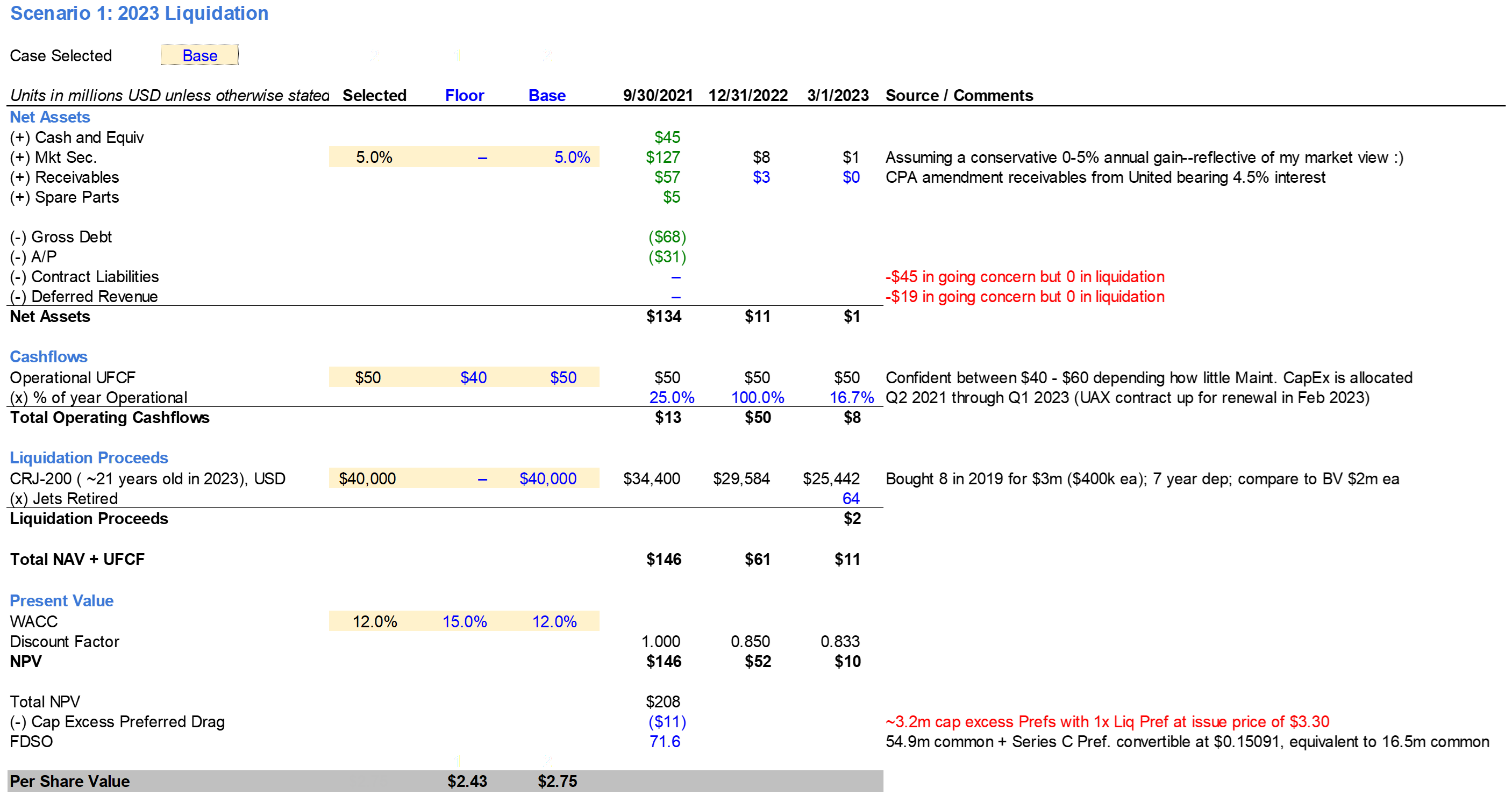

One critical development to call out upfront is: I took feedback from several fellow investors and commentors (very helpful so keep em coming!) and corrected some errors—the most material of which being that I was overly punitive by counting deferred revenue/contract liabilities in the liquidation case, which will increase NAV to ~$2.75 in the liquidation case. More later.

Scenarios update

In my previous post, I laid out four scenarios. Since United has now opted not to renew the contract, 2023 liquidation (case 1) has become my new base case, with the other options still as upside cases:

Renegotiate a new contract through 2026

Opting not to renew the contract by the time of option expiration does not necessarily mean they are out of the game. They could be renegotiating which makes total sense given how much (undeserved) upside HRBR has received from the deferred revenues, plus UAL’s plan to upgauge fully by 2026. A lower capacity agreement could still very much be in the works.Sell to another airline or UAL

HRBR has been testing CRJ-700s and 900s, and has begun training pilots for these larger jets, indicating an openness to upgauge.Repurpose CRJ-200 for cargo

HRBR has already indicated the desire to repurpose CRJ-200s for cargo, and are currently in the process of identifying a customer for the new 700/900s.

I elected not to model these upside cases in detail because it would be an exercise of false precision. I am extremely confident based on my previous modeling for scenarios 3 and 4 that the enterprise value would be at least 3-5x the current value in the neighborhood of $400m+ if either of these cases for going concern were to play out. The cargo case may be less lucrative than an acquisition, but basically any cash generated in a cargo operation would also be priced at negative value at the current price.

Q3 10Q update

Here are some highlights from the recent Q:

All time high revenue

Revenue of $72m in Q3 was a pleasant surprise, which is an all time high including all pre-COVID quarters re-ramping to full operations. Granted Q3 is a seasonally high quarter but topline strength is obviously always nice.Buybacks above $2.37

We can all agree HRBR’s IR team is non-existent/useless. However, if the most quiet IR team on Earth is buying back stock ABOVE $2.37, what are you doing sub $2? If you back into the average prices below and the price chart for July and August, you can infer they bought as high as $2.47.

CPA not renewed

United opted not to renew the agreement, meaning they are either cutting Air Wisconsin in 2023 or signing a newly negotiated contract (or maybe even acquiring Air Wisconsin or just its assets). I would think all cases are possible, but it’s still hard to pin a valuation for the upside cases, which is why I only modeled for the absolute worst case for liquidation in 2023, with the confidence that any positive news would mean a value significantly above that.

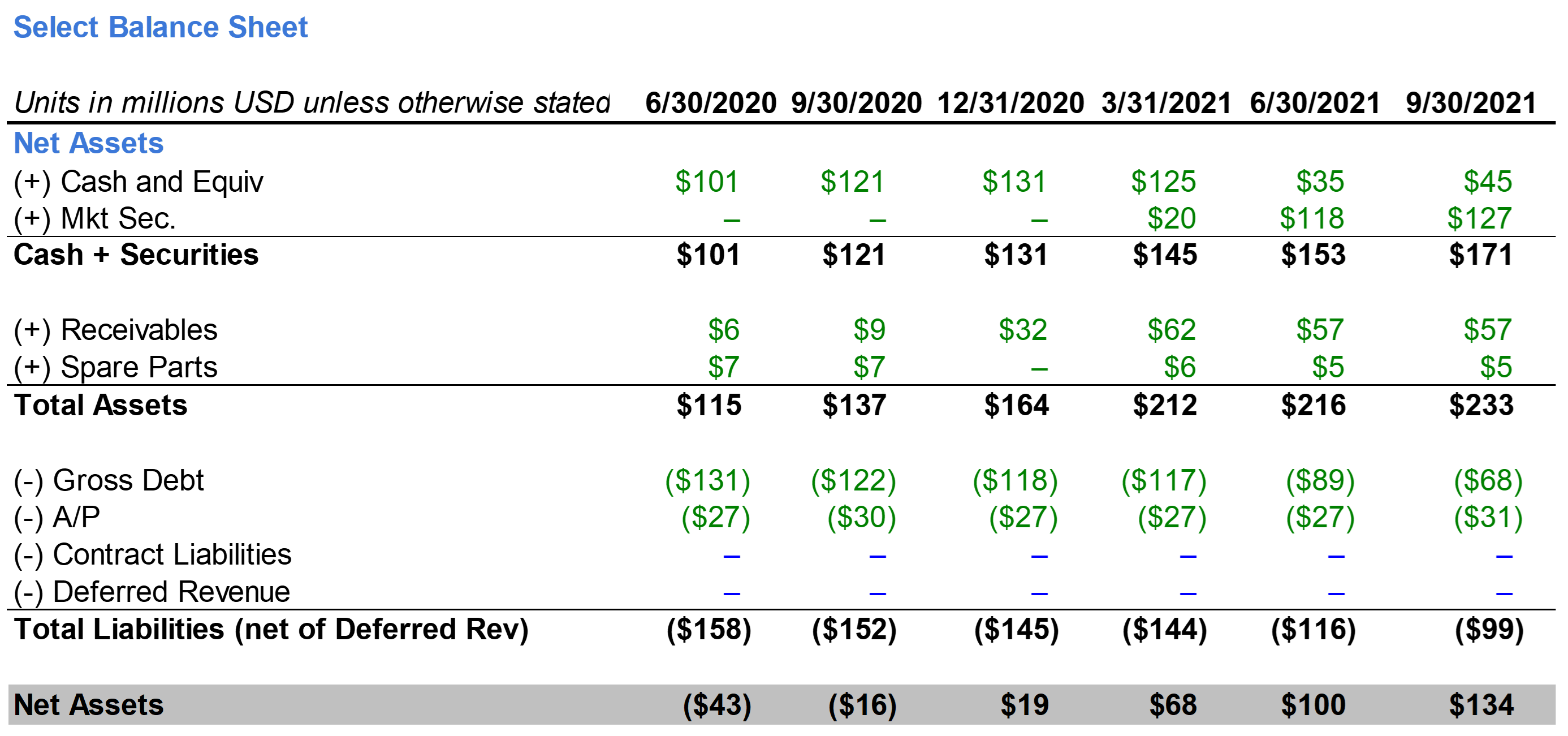

Balance sheet continues to steadily improve

HRBR continues to pay down loans (albeit with Uncle Sam’s PSP money) while improving its NAV position. $10m of SBA loan was forgiven by Uncle Sam as anticipated. Select balance sheet items improving below, excluding contract liabilities and deferred revenues in this liquidation case, which I will dive into detail later.

Liquidation case update

Again, I will not update scenarios 2-4 since these are upside cases and it’s pretty futile to model them precisely. I just know they will be WAY higher if this management pulls anything off, which I believe quite confidently they may be able to.

Therefore the only material valuation update is for the 2023 liquidation case. Especially since this is my new base case and the overall downside case, I wanted to be 100% sure for the absolute floor value for HRBR.

The main difference

In the event of a liquidation, the contract liabilities and deferred revenues (non-current version of contract liabilities) would not be counted against NAV, while HRBR’s notes receivables will be counted for NAV.

Explanation

Think of it this way. UAL is HRBR’s boss. They negotiated this CPA before COVID that said Air Wisconsin here is your fixed advance payment (LT note receivable at 4.5% interest), and then promise you’ll fly X hours and we’ll pay you per block hour on top of this advance payment. Cue COVID, Air Wisconsin basically flew under 20-50% capacity for most of 2020, which is WAY below what UAL signed up for aka UAL WAY overpaid—but there’s no “recourse” in liquidation, as in this should not be treated as a debt-like liability to HRBR.

That’s why HRBR records the current year “flying deficit”, if you will, under contract liabilities and non-current as deferred revenues. This checks out in the cash flow statements, you can trace how UAL paid cash upfront and owes on the notes receivable, but Air Wisconsin records this deferred rev/contract liability entry to indicate that they flew WAY less than contracted block hours and “owe” this ghost money to UAL.

In other words, HRBR has a claim on United cash that they negotiated pre-COVID, while HRBR recognizes that it did not fly enough to earn this cash so they mark it in liabilities, which they owe to UAL in the future.

Well the kicker is, the receivables matter in liquidation but the deferred revs don’t. In the regular event of continued operations, deferred revs would matter, and it would eventually sort itself out in say 2023, 2024 etc. once flying is back to normal and HRBR slowly earns back this deferred revenue. However in a liquidation, UAL already paid this cash/owes the rest in a receivable. However HRBR doesn’t “owe” any of the unearned revenue to UAL in real cash.

Analogy

An analogy that happens often in the music industry to help understand: label pays artist $20k advance to get him a studio and equipment and says we’ll pay $5 per 1,000 streams after the first 4 million streams, which is equivalent to the $20k advance. Turns out the music is complete trash and gets 500 streams total. The artist can just walk away with $20k (sorta). His accountant would record the 4 million minus 500 streams x payout rate as the “deferred revenue” he owes the label until he surpasses 4 million streams, but that’s if he keeps working with the label. The label can’t ask for that $20k back if his music just really sucks and neither the artist nor the label can really do anything at this point . Of course it’s more complicated than this but that’s the high level dynamic with HRBR and UAL.

Valuation

There’s also a small preferred drag of ~$0.15 which I didn’t include on the last update, but that’s less material.

Here’s the new valuation:

For the record, the floor case is what I think is the lowest humanly possible, which is frankly unrealistic if you go through the assumptions. This is just to ascertain what would happen in an absolute shitfest so I can confidently bet above that, i.e. SPY appreciates 0% the next 2 years, HRBR earns $40m UFCF which imo is not likely given their last few quarters and conservative maintenance Capex requirements for a liquidation case which really should require minimal capex since they’re running the equipment into the ground, $0 scrap value for the 64 jets, and 15% WACC even though historically it’s more like 8.6%.

Here’s the value waterfall on a per FD share basis:

As you’ll see, the majority of the value comes from the cash and marketable securities, which is ironclad real green cash and you can’t dispute has been steadily increasing the last few quarters from UFCF and Uncle Sam PSPs.

There have been arguments over how much EBIT or FCF the business can really generate, and how much scrap value is for the old CRJ-200 jets are. Hopefully this waterfall shows how immaterial those are compared to the MASSIVE CASH BALANCE sitting on the balance sheet.

The cap excess pref was pointed out by a commentor, basically due to the conversion price of the prefs, there is a ~3.2m pref cap excess that can be redeemed at issue price of $3.30 per pref, which is about $11m and equivalent to a $0.15 drag on the 71.6m FDSO.

Summary

HRBR is basically a heads you win big, tails you win small situation at the sub $2 price it’s been floating around.

You’ve got management buying back stock up to $2.47 (so far)

Net asset shell worth $2.02 by itself if business drops dead tomorrow

Numerous upside cases from renegotiated contract, a cargo play, an acquisition, all of which will multiply the current stock price

Steadily improving balance sheet that is held up by primarily cash

All time high revenue (and cash flow)

I also want to point out how uncorrelated HRBR is with the broader market downturn, AND the numerous COVID affected travel plays out there. This is a special situation play that is shielded from broader market movements.

This is still my largest position, and I’m excited and confidently holding through at least Feb 2023 or material news changes the thesis.

Caveat: I would definitely buy more if it weren’t already such an irresponsibly large position in my portfolio, holding simply due to portfolio construction considerations.

Catalysts

10K due 3/31/22

More details regarding UAL relationship released by United or Air Wisconsin

News of cargo customers

Flight data from Air Wisconsin’s new 700/900 jets

Additional certifications on FAA website

One last note:

Just to be extra sure, I’d encourage folks to also become registered shareholders, otherwise HRBR could (unlikely) pull another delisting if there are under 300 shareholders of record.

If you hold HRBR through a broker like TDA or IBKR, you are registered under “street name” and everyone in TDA for example counts as 1 registered holder.

There are several ways to become a direct registered holder, but the easiest and cheapest way is just to call your broker and ask them to do a direct registration system (DRS transfer) of 1 share from your broker to Computershare. Computershare doesn’t charge for incoming transfers and I believe IBKR is cheapest at $5 per DRS withdrawal. Some brokers charge a shit ton so definitely check before requesting. If you want to be cool or make this a memorable one you can also become registered by requesting a paper stock certificate for like $200 or so :)

Disclaimer: At the time of writing I am long HRBR.

The above references my opinion and is for information purposes only. I am not being compensated by any company or persons mentioned in this article. The opinions stated here do not represent my employer’s opinions. All information used is publicly available or reasonably obtainable and assumed to be factual. This is not intended to be investment advice. Investing in unregulated securities bears extremely high risk.

If you are going to become a registered holder to try to prevent an involuntary delisting, usually worth moving over at least >201 shares to preclude any reverse share split cash-out shenanigans!!!

Look at $TTSH holders of record history for reference….

What's your base case now that a 5-year contract has been signed? Thanks!