NTP: a timeboxed activist lawsuit Special Situation with incredible risk/reward

The best risk/reward options play I have ever seen, truly.

03/04/21 Trial Decision Update

Great news: IsZo won the lawsuit. I closed half my remaining 7.5 strike calls upon announcement at $4.50 (800% return in 4 months, $11 NTP spot) and rolled the remaining half into the March 19th 12.5 strike calls, in anticipation of the April 26, 2021 Special Meeting for shareholders to vote for IsZo’s board appointments. The presser notes “On September 11, 2020, IsZo delivered to Nam Tai verified requests to convene a Special Meeting from holders of approximately 40% of the Company’s outstanding shares – a number far in excess of the 30% requirement.” So this Special Meeting should likely go in IsZo’s favor as well.

-Fully Exited 3/8/21.

02/05/21 Trial Start Update

The trial began on 1/29/21, and NTP’s spot price already hit $8, my base case target—guess others are optimistic as well. I have closed my cost basis on the 7.5 strike calls at a price of $2.15 (330% return in 2.5 months) plus all 5 strike calls at a price of $4.00 (300% return in 2.5 months). Both are higher than my targets because of the 1 additional month of theta decay I baked in for conservatism plus higher than anticipated IV (140% vs my conservative estimate of 120%).

Summary

Nam Tai Properties, a commercial real estate developer in China, is being sued by IsZo, an activist investor, following poor management, allegations of corruption, and massive ownership dilution. While I have a neutral fundamental view of the underlying company’s value, this lawsuit setup has presented a special situation with EXTREMELY lopsided risk/reward in NTP’s call options.

Not only is this a very simple outcome to model, it is also time bound. In addition, several data points indicate the likelier outcome of a successful lawsuit, and most importantly, the risk/reward of current call options prices are simply astoundingly attractive. This is basically a big math question and the answer is:

I conservatively expect 70% risk-adjusted returns within 4 months, with potential for 440%+ returns on the upside.

Sections:

Background

Valuation

Catalysts

I: Background

Nam Tai Property ($NTP) owns, develops, and operates industrial technology parks in China. Its flagship property is InnoPark, a repurposed factory outside of Shen Zhen (China’s San Francisco).

Its largest minority owner is a “Kaisa Group” who for the past few years has overseen a steep decline in share price despite the InnoPark property being not only quite a valuable piece of land but also the development itself having high potential for the tech manufacturing needs of booming Shen Zhen.

Kaisa enters the chat

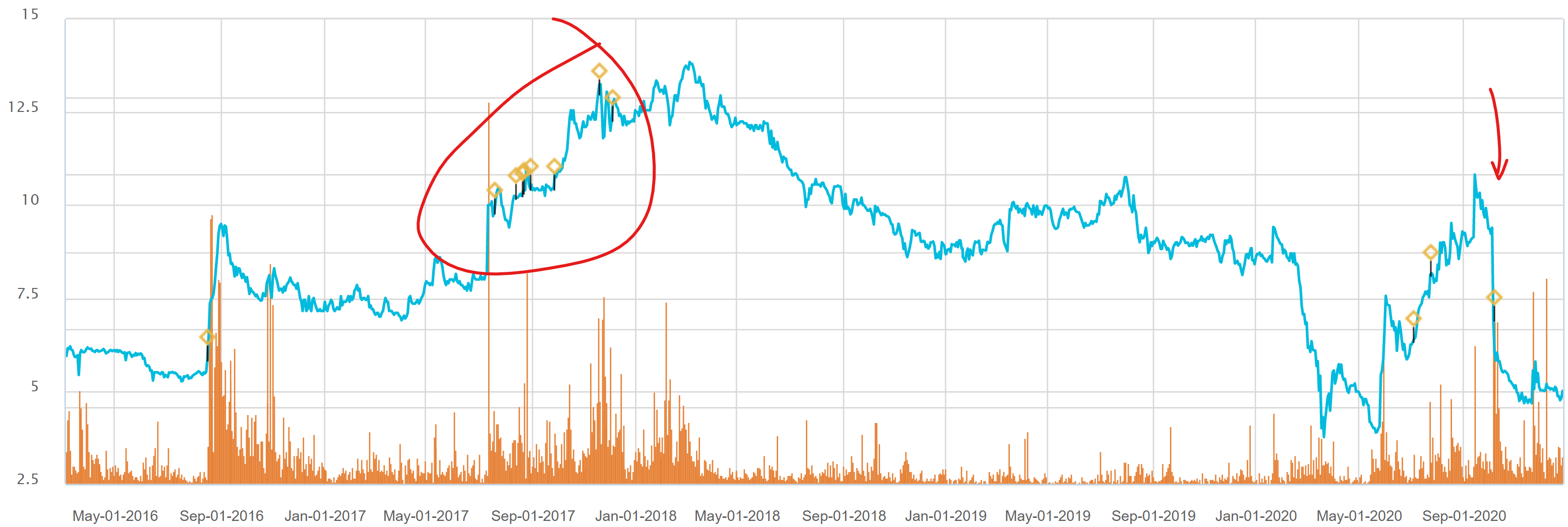

Looking at NTP’s price chart, you will notice a cluster of insider buys in 2017 (red circle) where Kaisa built its position to become the largest minority owner, followed by a steady decline in excess of 75% in the stock price over 3 years finally to COVID lows.

As stock price began to recover in mid-2020, the company in October 2020 (red arrow) suddenly raised a MONSTROUSLY dilutive PIPE issuing 18.6m shares vs. the existing 39m shares, which represented a 40% dilution, for purportedly paying down debt that was at risk for early cancellation. And guess who led the PIPE and received 16m of those shares? Yup it’s Kaisa.

Now this is already pretty sketchy but let’s look a little deeper at Nam Tai’s management. Notice that Kaisa is all over the board and C-suite, and in particular Kwok Ying Chi the CEO and Chairman of the Board, is the younger brother of Kwok Ying Shing , Kaisa’s Chairman.

This whole thing reeks of Kaisa and Kwok family nepotism, which would be less of a problem if the company was run well, but other cracks merged in the edifice:

First of all, the structure of the PIPE already raises eyebrows—the largest minority owner just issued itself 1/3 of the fully diluted shares to go from a 24% owner to a 44% owner?

Not only that, the fact that the board needed to raise capital to pay down debt that triggered protective covenants made the whole thing even more sour.

Plus, why hasn’t NTP managed to create shareholder return over the years with such a valuable collection of assets and a burgeoning tech hub nearby?

Finally, all this happened with the backdrop of Kwok resigning as CEO a month earlier in September for “personal reasons”—can I say hmmmmm.

As expected, upon announcement of the PIPE share price was decimated and tanked 60%+ to nearly all time lows of $5, where we are today.

IsZo to the rescue

An alternative asset manager in New York named IsZo with roughly $90m AUM has been holding NTP since 2014, and further built up its position in 2020 to a roughly 10% stake in NTP. IsZo is a single manager hedge fund ran by an individual named Brian Seehy, a UC Berkeley grad, who was previously an MD at Black Horse Capital, a real estate investment and advisory firm.

As the second largest minority shareholder behind the Kaisa Mafia, IsZo was obviously displeased with the massive dilution event and share price destruction, and put out an activist campaign to invalidate the PIPE and also replace members of the board. The full campaign can be found here, and NTP’s response can be found here. Court hearings begin 1/29/21 and are scheduled to conclude by early March 2021.

II: Risk Reward Valuation

This whole background was honestly quite fascinating to me, and who doesn’t like an investment with an entertaining origin story (check out this post on HRBR for the weirdest background I’ve ever seen). More importantly, how can we capitalize on this opportunity?

I like this unique setup because it is time-bound, structured, simple, and the risk/reward is so absurdly asymmetric. The thesis is simply around risk and reward on the IsZo lawsuit outcome.

This trade is a little different than the fundamental investing approach I usually take. I like this opportunity not because of the fundamentals of NTP as I am not a real estate valuation expert—disclaimer: I did take a look at both management’s valuation plus IsZo’s take, and I am satisfactorily convinced that this piece of land exists and is not garbage, which is enough of a prerequisite for me on this front.

Rather, I am focused only 3 things:

The likelihood of each of 2 outcomes of the lawsuit

The expected payout for each outcome

The price of risk

Lawsuit outcome probability

The lawsuit could end in 2 ways: either the PIPE is canceled, or it is not, and we will know by early March 2021.

I am inclined to believe the lawsuit is more likely than not to succeed primarily because:

IsZo has a ton of capital tied up in NTP and the downside to Brian Seehy would be astronomical, so you know he is aligned with shareholders. Since 2014 IsZo has had in excess of 30% of its portfolio in NTP. As of 11/14/20 per its 2020 Q3 13F, NTP had only 3 positions, and NTP accounted for 49% of its AUM.

IsZo 2020 Q3 13F The hearing is being held in the British Virgin Islands. The BVI court is historically a shareholder friendly court. I am not a legal expert but in my limited perspective, I believe the nepotism, mismanagement, and detriment to shareholders are all quite apparent not only in the stock price but in the untimely resignation of Kwok and the egregiously nefarious terms of the PIPE. Given the BVI court’s history and how unabashed Kaisa Group’s actions were, I think the suit is likely to succeed.

For the base case, let’s call it a 60% chance of winning and 40% chance of losing in the spirit of conservatism, though I do think the odds are more favorable than that.

Expected payout

Similarly there is two payout scenarios:

If the PIPE is reversed, the 16m shares issued are nullified, and the dilution is reversed. Based on the current price of $5, the un-dilution would bring the price back up to ~$8, which we can use as the base case. Realistically, the favorable outcome would lead to price appreciation much beyond that due to the board replacements that IsZo is also trying to implement, plus investor sentiment on the win, but let’s assume a $8 base case for conservatism.

If the lawsuit fails, I do not think it is likely that the stock price can fall much further than $3, which is the all time low spanning 25+ years.

This type of payout structure lends itself to a call option, so let’s see how the risk is being priced.

Price of risk

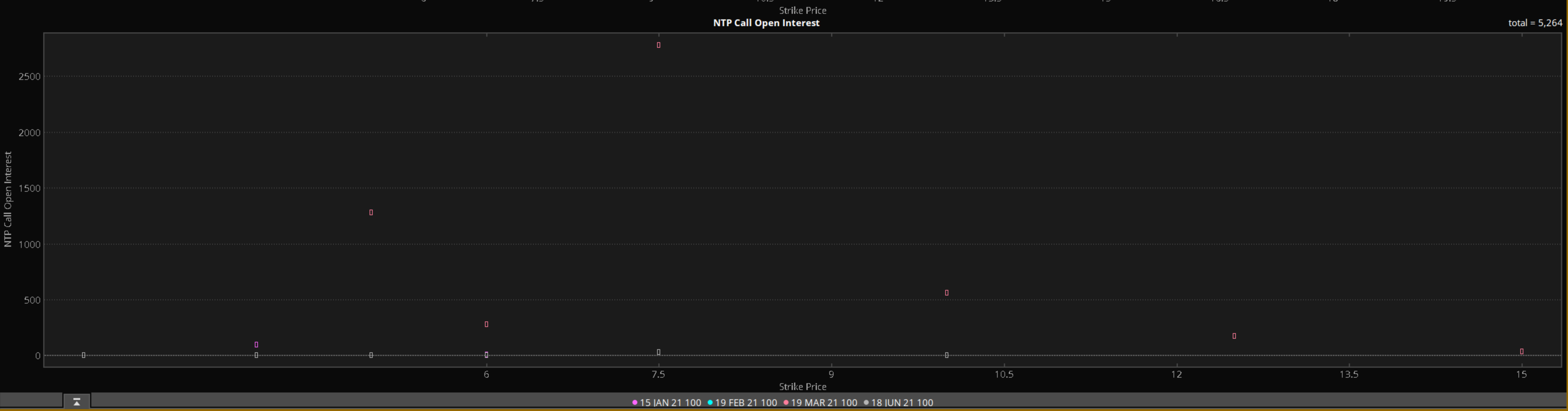

One thing I love about this trade is that it is time-defined, making option product selection very easy. We know the trials start on 1/29/21, and will end in early March 2021, so from the option chains available, the 3/19/21 expiry is the only one that makes sense.

While I was happy to see that the Open Interest for this expiry is significantly higher than all the other expiries, meaning some people were already on to this trade, it also slightly concerned me about how priced-in the risk was.

Assumptions

But to my amazement the prices were still low. The spot price is $5. I set price slices for each of my cases: $3 lose case, $8 base win case, $10 upside win case. I assumed a 30% increase in IV, and a sell date of 3/1/21. The current IV is around 90% and the median in 2020 looks to be ~135%, so this is not implausible given the vol buildup before the trial result announcement.

I only looked at the 5 and 7.5 strike because anything below the current spot price of 5 would produce unfavorable returns compared to the 5, and anything above 7.5 was a bit too risky given my base case is 8 and upside case is 10.

5 Strike

The $5 strike was going for $1.00 each. This translates to a $5.80 spot breakeven on 3/1/21 based on the default Bjerksund-Stensland model on TD-Ameritrade’s ThinkorSwim, which I love btw. For the base case of $8 the expected pay out is 200%, with the upside case at $10 paying out 400%. Obviously the lose case would result in a 100% loss.

7.5 Strike

The $7.5 strike had the highest open interest yet was only $0.50 each. This translates to a $6.30 spot breakeven on 3/1/21. For the base case of $8 the expected pay out was 170%, with the upside case at $10 paying out 440%. Again, the lose case would result in a 100% loss.

The expected payout based on our scenario probabilities (60% win, 40% lose) are the following:

5 strike

0.6*200% + 0.4*-100% = 80% base case

0.6*400% + 0.4*-100% = 200% upside case

7.5 strike

0.6*170% + 0.4*-100% = 60% base case

0.6*440% + 0.4*-100% = 220% upside case

Both are ridiculously good expected returns, and as one would expect intuitively the 7.5 strike rewards higher convexity. Ultimately I chose to buy both the 5 and 7.5 strike in a equal weighted 1:2 ratio, for some conservatism. Still, this risk reward in this situation is astounding.

Overall, I very conservatively expect 70% risk-adjusted returns within 3 months, with potential for 440%+ in the upside case.

III: Catalysts

The catalysts here are simple because it is such a structured process:

1/29/21: Trials begin: I expect a press release which will increase awareness.

Early to Mid March: Trial results will be released.

In between: IsZo may very well release more documents and promote its activist campaign.

Disclaimer: At time of writing I am long NTP.

The above references my opinion and is for information purposes only. I am not being compensated by any company or persons mentioned in this article. The opinions stated here do not represent my employer’s opinions. All information used is publicly available and assumed to be factual. This is not intended to be investment advice. Investing in unregulated securities bears extremely high risk.